Every year you go through the same thing — filing your taxes. Why? Because you need to know if your employer (or you) paid enough of your wages to the IRS and whether you get a refund.

But how did your money get to the IRS in the first place? Unless you are self-employed, your employer withheld a portion of your paycheck each period and sent it to the agency.

While getting all the money yourself would be nice, the IRS knows you probably won't remember to save enough to pay your taxes each year. So the federal government designed a system of partial payments throughout the year based on guesswork about your earnings.

It isn't perfect, but it's better than owing a colossal tax bill every year.

How Does Tax Withholding Work?

Employers must withhold a portion of each employee's salary and use it to pay income tax on the employee's behalf, along with Social Security and Medicare taxes. If you pay state income taxes, the employer withholds that, too. The only exception is for the rare tax-exempt employee.

The federal tax laws make employers responsible for withholding and paying taxes. If you are self-employed, the law requires you to do something similar by paying quarterly estimated taxes.

How Much Should Employers Withhold?

Withholding varies according to the amount of employee wages and the withholding information provided on the employee’s W-4 form.

If the employer withholds too little, the employee faces a tax bill in April. If too much is withheld, the employee receives a refund but cannot access the funds beforehand.

When you fill out your W-4, you can only claim the number of allowances you are entitled to. You can't claim an allowance just because you don't want taxes withheld. If you don't request enough withholding, the IRS intervenes with your employer by issuing a “lock-in letter” that supersedes your W-4 selections.

You also receive a copy of the letter. Still, you can fix things by submitting a new W-4 and a statement supporting claims that would decrease your withholding. However, once the IRS issues the letter, you cannot reduce your withholding unless the agency approves.

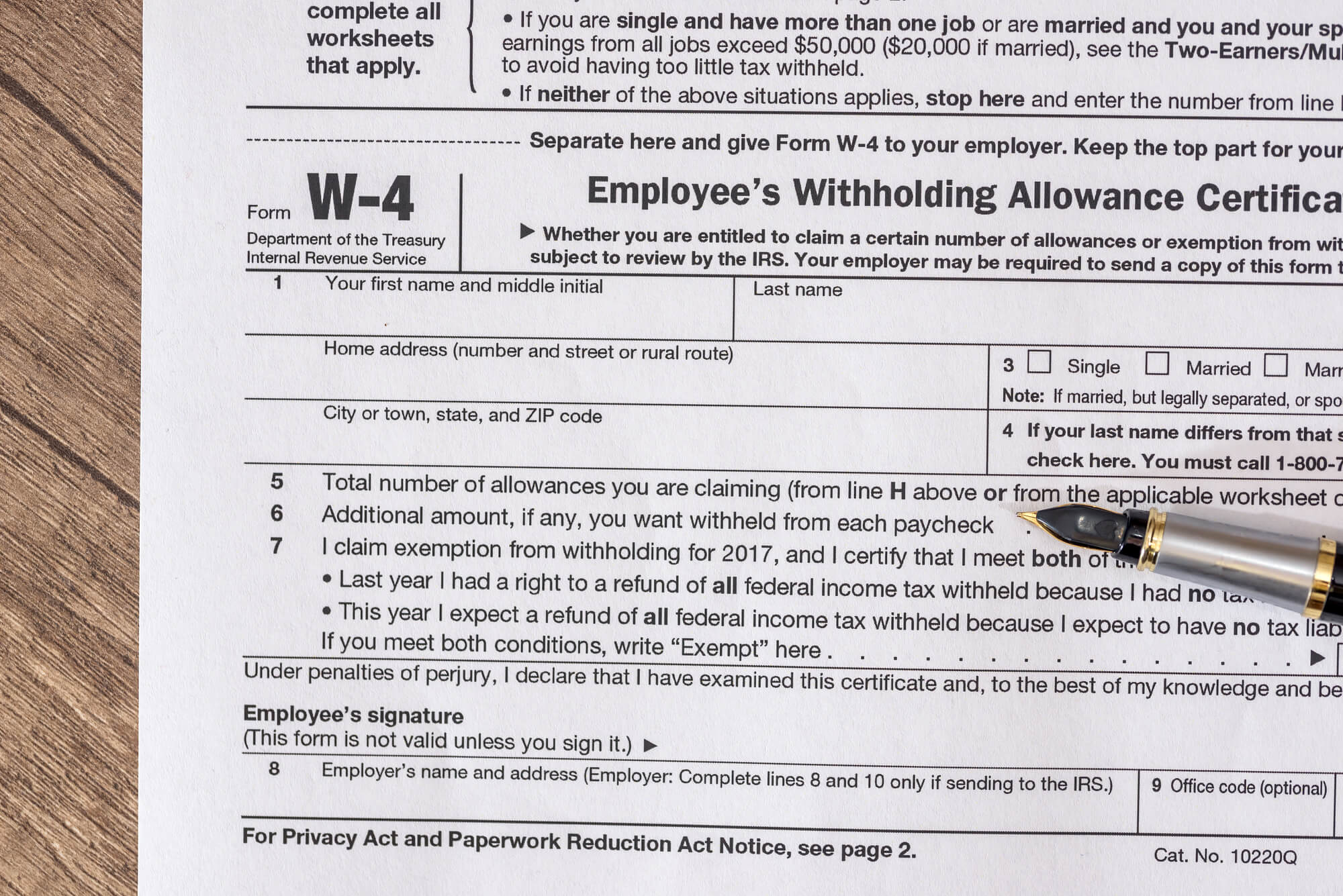

Filling Out the W-4

As a new employee, you must submit a W-4 to your employer. This is your chance to minimize the amount of withholding without setting yourself up for a huge tax bill. It's tempting to ask for more withholding as a form of savings account, but you are just giving Uncle Sam an interest-free loan of your money.

You’re better off getting a small refund or owing a small amount. Then you can take advantage of more earnings throughout the year.

The W-4 form asks you to state the following:

- Your filing status - single, married filing jointly, etc.

- The number of withholding allowances you claim

- Any additional amount you want to be withheld

You can claim allowances for yourself, your spouse, and any dependents and qualified tax credits. The potential tax credits include:

- Child tax credit

- Education credit

- Adoption credit

- Credit for the elderly or disabled

- Foreign tax credits

- Retirement savings credit

- Prior year AMT credit

- Child and dependent care credit

- Credit for home mortgage interest

- General business credit

- Earned income credit

You are not required to fill out a new W-4 every year, but it's a good idea to do so if you anticipate a life event, like:

- Getting married or divorced

- Having or adopting a child

- Changing the income you have that isn't subject to withholding, like interest, dividends, and capital gains

- Retiring from a job

- Buying a new home

- Increased tax-deductible expenses for medical bills, taxes, interest, charitable giving, jobs expenses, or dependent care expenses

If this all sounds strange, you haven't filled out a W-4 for quite a while. The IRS revamped Form W-4 in 2020 to make it more user-friendly and gather more information than previous W-4 forms.

For example, the form now asks about other jobs you or your spouse held and information on the non-W-4 income you receive and tax deductions you plan to take.

Take note: you only need to include this information on the W-4 of your highest-paying job. Also, consider changing your withholding if you get a raise, take a second job, or your income increases enough to move you to a higher tax bracket.

You can make adjustments anytime. Check with your employer regarding policies and procedures. And remember, any new withholding goes into effect for future paychecks only, so if you adjust withholdings late in the year, the impact may not be as significant as you require.

Where to Find Your Current Withholding

Your pay stub should show any withholdings from your earnings, including federal and state tax withholdings, Social Security, Medicare, and other withholding or payment such as health insurance.

Your withholding is based on your income tax rate, plus 6.2% of your income up to $147,000 in 2022 for Social Security and 1.45% for Medicare.

For a rough estimate of your tax withholding, use the online tax calculator from the IRS. You need pay stubs for all jobs, including your spouse’s, and any other income information like side jobs, self-employment, and investments. You also need your most current tax return.

The tool is ineffective, however, if you have a pension but no job, if you hold non-resident alien status, or if you have a complex tax situation.

What If Your Employer Needs to Correct Withholding?

If your employer withholds the incorrect amount, they could reduce or increase withholdings in subsequent paychecks until it is correct. Depending on the original form filed, they must also file corrected Forms 941-X or 944-X for each employer.

The correction requires the amount reported initially, the corrected amount, the difference between the two, and some business information. The employer must send an updated form for each affected employee.

Need Help? Ask Top Tax Defenders

A single person with one job and no other allowances has it pretty easy. But once you get married, have children, or qualify for one of many credits offered by the federal government, filling out your W-4 can get kinda tricky.

If your withholding is too low, you owe a hefty tax bill. You get a fantastic refund if it's too much, but you could have used that money throughout the year.

Contact us for assistance or to answer any questions.